Small-Cap Stocks And What Consistent Market Winners Get Right

India’s small-cap market has a recurring pattern that every seasoned investor has witnessed: a company announces an ambitious capex plan, a new vertical, or a government-linked opportunity, and the stock responds immediately. Volume spikes. Retail interest floods in. Valuation multiples stretch.

Then, six to twelve months later, the follow-through never comes. Margins are missed. Order books remain thin. Management commentary grows vague. The stock gives back everything and then some.

This is not a new story. It is the dominant story of small-cap investing in India. And yet, the market continues to price announcements as if they were outcomes.

The real question for sophisticated investors is not which company made the most compelling announcement; it is which company will actually execute on it.

“Markets love announcements. But they eventually punish non-delivery — and in small caps, that punishment is swift and unforgiving.”

The Announcement Trap

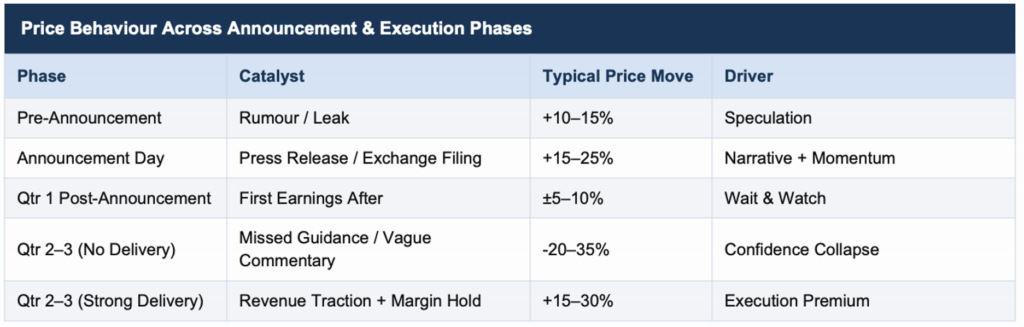

In India’s small-cap universe, broadly defined as companies with market capitalisation below ₹5,000 crore, the announcement premium is well-documented. Capital expenditure plans, MoUs with government bodies, entry into new product categories, or franchise expansion narratives regularly drive 20–40% short-term price moves.

What this signals is a structural bias in how retail-heavy markets process information. In the absence of deep institutional coverage and analyst follow-up, narratives fill the vacuum. A company’s story becomes its stock price — at least temporarily.

The problem surfaces when the first 2–4 quarterly earnings cycles post-announcement fail to show corresponding traction. Revenue lines don’t move. Working capital deteriorates. Capex timelines slip from ‘this fiscal’ to ‘H2 next fiscal’ to ‘under review’.

Value erosion at this stage is not gradual. Investor confidence, once shaken in small caps, unwinds rapidly. The same liquidity that drove the stock up becomes the exit pressure that drives it down.

CHART 1 — Small-Cap Stock Behaviour: Announcement Phase vs. Post-Execution Phase

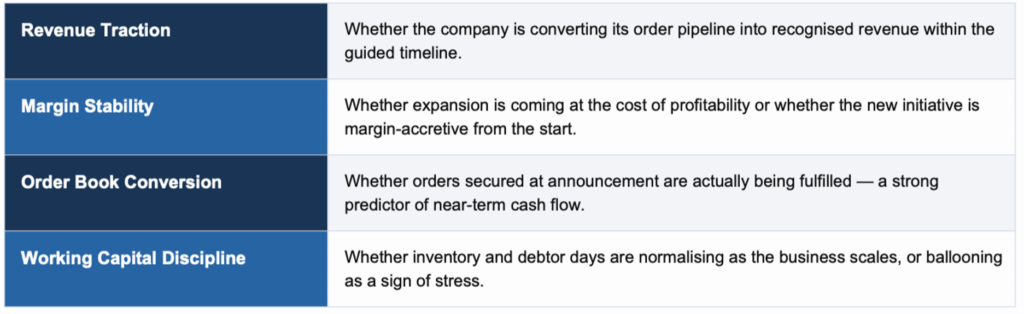

The First-Phase Execution Window

The most critical and most underappreciated period in a small-cap stock’s lifecycle is the first 2–4 quarters after a major strategic announcement. This window is when promises are tested against operational reality and when the market begins separating execution-capable businesses from story stocks.

The real inflection point isn’t the announcement; it’s the first evidence of execution. Investors who understand this can position ahead of the re-rating, rather than chase the hype.

Companies that demonstrate clean execution across even two of these four metrics in the first post-announcement quarter attract a different class of capital and a different valuation floor.

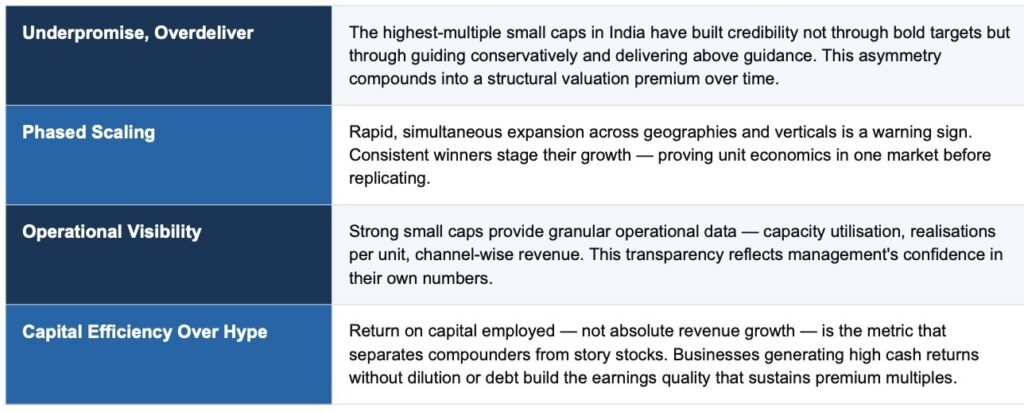

What Consistent Market Winners Get Right

Across market cycles, a clear pattern emerges among small-cap companies that sustain a long-term valuation premium. They do not simply outperform; they outperform consistently and predictably. The underlying behaviours are remarkably similar.

“Consistency compounds valuation multiples. One strong quarter moves a stock. Four consistent quarters re-rate a business.”

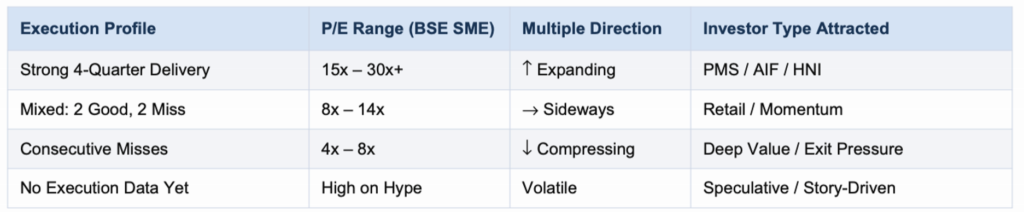

Chart 2: Valuation Multiple Behaviour by Execution Consistency

Why the Market Is Changing — And Faster Than Most Realise

Five years ago, a compelling narrative and a credible promoter were often sufficient to sustain a small-cap stock’s premium. Today, that equation has fundamentally shifted.

Three structural changes are reshaping the information environment for small-cap stocks in India. First, data access has democratised dramatically; quarterly results, exchange filings, and management conference call transcripts are now indexed, analysed, and distributed within hours of release. Second, the rise of PMS and AIF capital targeting the small-cap segment has introduced institutional-grade scrutiny to a market previously dominated by retail sentiment. Third, information cycles have compressed — a guidance miss that once took two quarters to get priced in now moves the stock within the week.

The implication is direct: narratives are no longer enough. Proof-of-execution is now priced in faster than ever. The market’s patience for story stocks without earnings delivery has shortened considerably.

This is not merely an academic observation. It is a structural shift in how alpha is generated and sustained in the small-cap space.

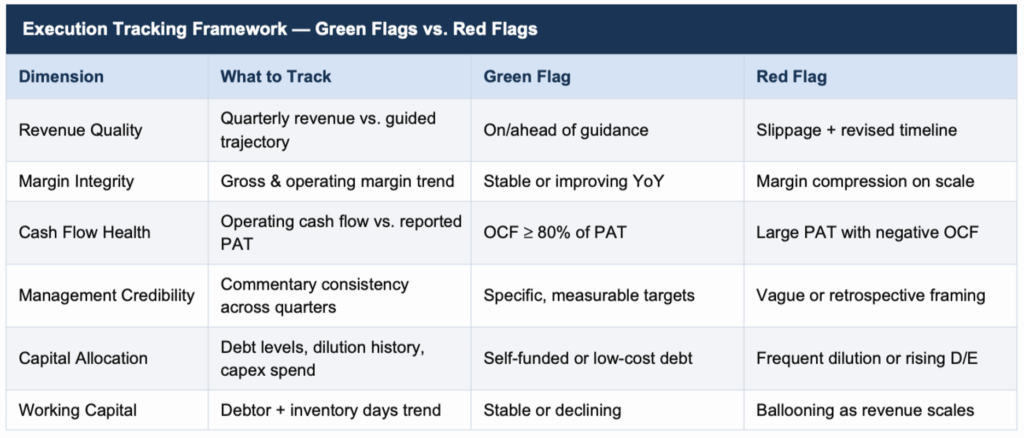

Investor Lens: An Execution-First Framework for Small Caps

For institutional investors, PMS managers, and serious market participants evaluating small-cap opportunities in India today, the analytical lens must shift from ‘what is the story?’ to ‘where is the proof?’

A practical execution-tracking framework should be built on three pillars:

In today’s market, execution is the new alpha. Investors who build systematic frameworks to track delivery, rather than react to announcements, position themselves to identify re-rating opportunities before they become consensus.

The Road Ahead: Execution-First Is India’s Next Small-Cap Cycle

India’s small-cap market will continue to generate significant wealth creation opportunities. The structural drivers, rising consumption, formalisation of supply chains, digital distribution, and domestic manufacturing growth, are secular and multi-decade in nature.

But the next phase of small-cap returns will not be distributed uniformly. As institutional participation deepens, as information asymmetry narrows, and as the quality of market participants improves, the gap between execution-first businesses and narrative-first companies will widen in returns, in valuation multiples, and in investor base quality.

The companies that build credibility through consistent delivery in their first phase of execution, on revenue, margins, cash flow, and capital discipline, are the ones that will attract permanent, sophisticated capital. Those who live on announcements alone will find the market’s patience increasingly short.

“In the long run, markets don’t reward promises. They reward proof.”